Your Health Insurance: A Hidden Premium Increase

Oct 25, 2016

Every year around this time I write about health insurance. PLEASE SHARE THIS BLOG WITH A COLLEAGUE, A FRIEND, OR ANYONE ELSE YOU THINK WOULD BENEFIT. (For last year’s post on choosing health insurance, click here.)

At this time of year, many of us face choices about health insurance plans for the upcoming year. Depressingly large premium increases have been typical, and recent news suggests 2017 will be no exception. And my own personal experience suggests that you may find yourself getting socked even more with a hidden increase: an increase in your calendar year deductible (CYD).

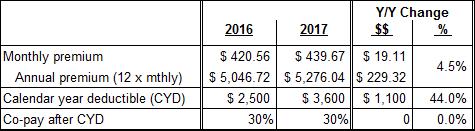

Consider this example, comparing your 2017 insurance costs to 2016:

The good news: Your premium “only” goes up 4.5%, which looks mighty good these days. Now the bad news: Your CYD is going up by $1,100. How much will that actually cost you?

Let’s make the simplifying assumption that 2017 will either be a “good” or a “bad” year for your total medical expenses – i.e., either less than your 2016 CYD of $2,500, or more than your 2017 CYD of $3,500. If 2017 is a “good” year, the $1,100 increase in your CYD costs you nothing. But if 2017 is a “bad” year, you’ll pay $770 more out of your own pocket than you would’ve paid out under the 2016 plan – i.e., the full $1,100 increase in your deductible less the 30% co-pay you would’ve had to pay under the 2016 plan. This higher deductible is effectively a premium increase.

To determine the likely cost of this premium increase, use a statistical concept called an expectation, which is the sum of each possible outcome, times the probability of that outcome occurring. If you believe your chance of a “good” medical expenses year is 60% and 40% for a “bad” year, your expected cost in 2017 due to the increased CYD is:

(60% x $0) + (40% x $770) = $308

That $308 increase in your expected medical costs means that the expected % increase in the cost of your insurance isn’t the 4.5% you originally thought, but 10.6%! (i.e., the $229.32 premium increase, plus $308 in expected additional co-pays, or $537.32, which is 10.6% of the 2016 annual premium of $5,046.72.)

So when you’re considering your 2017 health insurance alternatives, don’t consider just the increase in your monthly premium – pay attention to the other ways your cost of healthcare might change.

“Painting with Numbers” is my effort to get people to focus on making numbers understandable. I welcome your feedback and your favorite examples. Follow me on twitter at @RandallBolten.

Here’s another deceptive alternative that some insurers will offer: A lower co-pay – like 10% or 20% instead of 30%, or a low straight dollar amount like $25 for an office visit – once you’ve exceeded your CYD. That may sound like a great deal, but if your out-of-pocket maximum exceeds your CYD by a tiny amount like $100 or $200, that lower co-pay has virtually no value at all.

Other Topics